16 / 60

16 / 60

14

January 2020

as living conditions improve. Domestic gas consumption is

forecast to grow approximately 10% annually in the next

decade, supported by government efforts to diversify out of coal

into cleaner alternatives.

One factor setting Vietnam apart is its emergence as a

global manufacturing hub. Manufacturers are setting up shop in

Vietnam, attracted by the competitive local cost environment.

The structural shift in Vietnam’s economic make-up will push it

along a more gas-intensive growth trajectory.

A narrative around supply tightness is emerging – while

Vietnam has gas fields, production facilities and processing

infrastructure, it also has finite resources. Vietnam’s domestic

gas production is on a sharp decline curve after 2020 as

existing fields are exhausted, precisely at the same time when

energy demand is ramping up.

Under its gas industry development plan, Vietnam is

looking at LNG imports to bridge the shortfall. An estimated 10

LNG terminals are in the pipeline.

2

This includes Vietnam’s first

LNG terminal in the southern port of Thi Vai, operated by

PetroVietnam and due for completion in 2022.

3

In another

landmark project, Vietnamese NOC Petrolimex, in partnership

with Japan’s JXTG, is looking to build an integrated LNG

terminal and power plant in the southern coastal province of

Khan Hoa.

4

Vietnam’s biggest challenge is financing its ambitious gas

infrastructure program with the public debt/GNP ratio close to

its ceiling level. Major LNG projects will have to compete with a

host of other proposed infrastructure projects to secure

government approval. The best hope is for foreign capital to

help fund an LNG infrastructure program. Established players

like Japan and the US are taking a serious look at Vietnam as a

potential new customer market to sell LNG.

Philippines

Strong economic growth, a large population and a national

policy focused on decarbonisation and energy diversity are

supportive demand drivers for LNG in the Philippines.

Similar to Vietnam, there are domestic supply concerns.

According to Department of Energy (DOE) estimates, the

offshore Malampaya gas field has less than five years of

available resources. Malampaya is the main source of natural

gas for Luzon, the most populated island in the Philippines

with more than 20 million people.

To secure the future of existing gas power stations and

create a foundation for additional plants, the Philippines is

turning to LNG. Philippine utility First Gen Corp. is poised to

build the first LNG import terminal in the Batangas province

before the Malampaya gas field reserves deplete in 2024. There

is Japanese interest with JGC Corp. identified as preferred

engineering, procurement and construction (EPC) contractor

and Tokyo Gas likely to take a 20% stake in the project.

5

Manila-based fuel retailer Phoenix Petroleum is in talks

with the Philippine National Oil Co. to develop a US$2 billion

LNG hub.

6

Like other emerging LNG projects, this is more than

simply building an LNG import terminal. It will likely include

gas pipelines, processing and other gas network infrastructure.

US project developers are looking at the Philippines closely.

One potential investor is Fortress Energy, which is currently in

talks with the DOE regarding an integrated onshore LNG import

terminal and gas power plant.

7

The US LNG model is attractive

given its ability to provide customised, flexible solutions ranging

from gas supply, conversion of existing plants into gas-fired

assets and development of Greenfield LNG power assets.

None of this is without challenges and risks. The

Philippines has courted LNG for several years. In 2015,

Australia’s Energy World Corp. (EWC) was close to building an

integrated LNG import hub and gas power plant in Quezon

province. The project has yet to materialise, with reports of

financing bottlenecks, regulatory barriers and issues over

transmission arrangements.

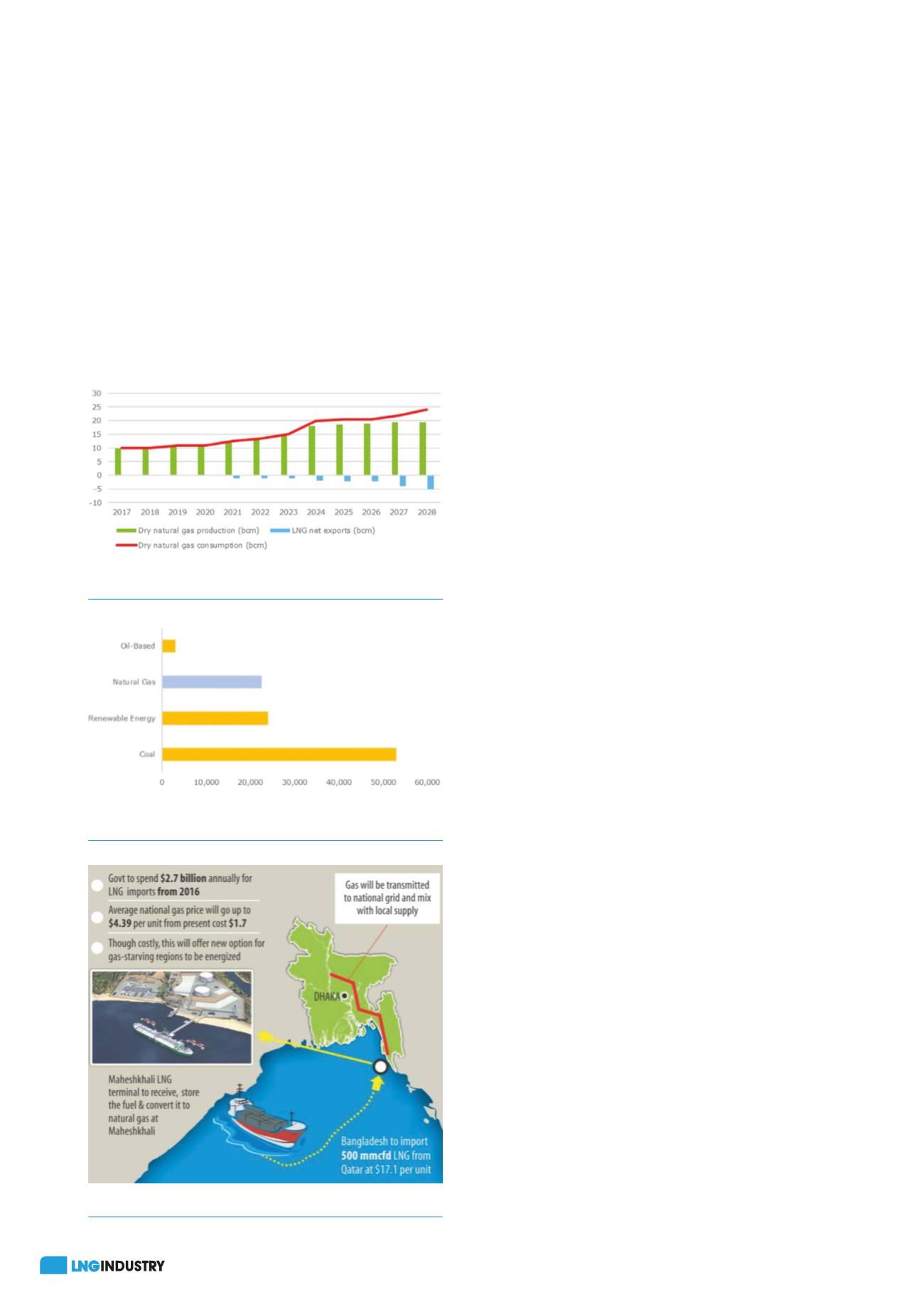

Bangladesh

A fast growing, South Asian emerging market economy with a

population of 150 million, Bangladesh is looking to develop

its gas industry, in partnership with overseas investors. It is a

familiar story of declining domestic gas output twinned with

rapidly growing demand and a need to diversify out of coal.

Figure 1.

Insufficient gas production pushes Vietnam to

LNG (source: EIA, Fitch Solutions).

Figure 2.

Philippine power generation fuel mix, 2018 (GWh)

(source: Philippine Department of Energy).

Figure 3.

Bangladesh tilts towards LNG.